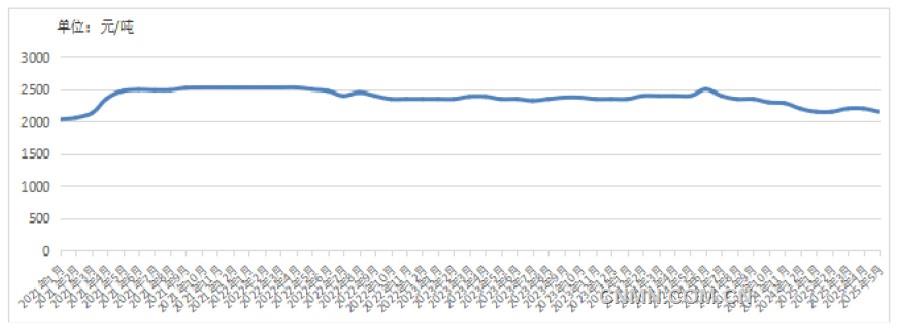

Trend Chart of Panzhihua 20# Titanium Ore Prices from 2021 to May 2025

Note: Prices are ex-factory prices excluding tax

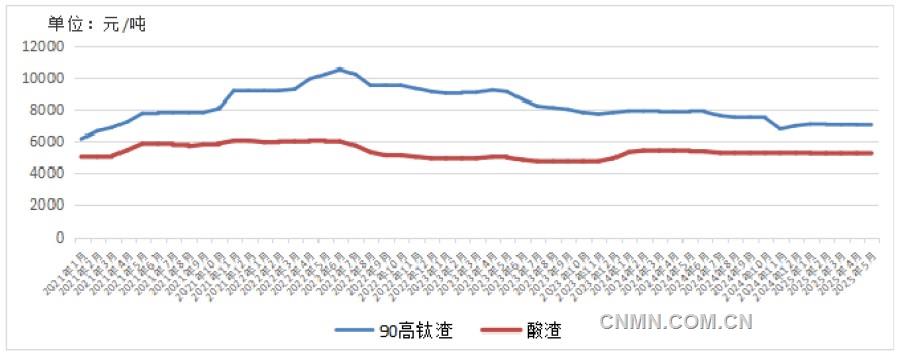

Trend Chart of Domestic Titanium Slag Prices from 2021 to May 2025

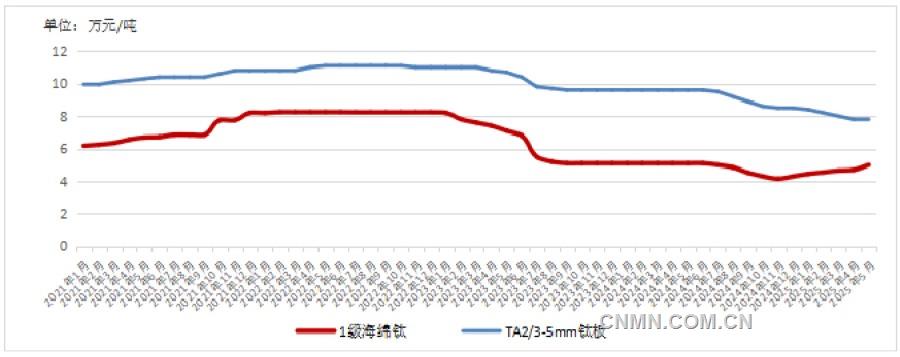

Trend Chart of Domestic Sponge Titanium/Titanium Plate Prices from 2021 to May 2025

Data Source: China Nonferrous Metals Industry Association, Titanium Zirconium Hafnium Vanadium Branch

Review of Domestic Price Trends

In May, the domestic titanium ore market showed a trend of first suppression and then recovery, with overall stable but weak performance. This was particularly evident in the Panxi region. In early May, due to the continuous decline in downstream titanium dioxide prices and a drop in operating rates, market demand weakened, leading to a panic-induced price drop. Among them, medium and small miners lowered their quotations by about 100 yuan/mt, while the price of medium-grade ore fell by around 130 yuan/mt, and large mines also reduced their prices by 100 yuan~150 yuan/mt. In late May, as some downstream enterprises resumed production, the demand for titanium ore rebounded slightly, and market confidence gradually recovered, with some medium and small miners in the Panxi region raising their quotations slightly.

In May, some imported titanium ore prices were also relatively weak. Affected by the decline in some domestic titanium ore and downstream product prices, there was significant pressure on the sales of imported titanium ore, with some transactions stalling, and imported ore prices saw slight adjustments. At month-end, Mozambique titanium ore prices stood at $370/mt, while Nigerian titanium ore ex-factory prices including tax ranged from 2,050 yuan~2,150 yuan/mt. The market was in a stalemate, with downstream buyers generally adopting a wait-and-see attitude.

In May, the titanium slag market exhibited a pattern of "weak and depressed acid slag, high titanium slag under pressure but relatively stable." Downstream enterprises did not conduct centralized tender purchases in May, and high titanium slag prices continued to follow the April market transaction prices. Although raw material costs pulled back slightly recently, high titanium slag producers still operated at a loss, showing low enthusiasm for production, with most enterprises cutting or halting production. The acid slag market had low production activity, with relatively small output, and some enterprises experienced inventory accumulation. Acid slag plants in Yunnan were basically shut down, while those in Panzhihua only maintained production for their own downstream factories. A few acid slag plants in north China maintained minimal production, resulting in a significant reduction in overall supply.

In May, domestic sponge titanium prices stabilized at a relatively high level. At the beginning of May, grade one sponge titanium prices stabilized at 50,000 yuan/mt with bulk transactions. Some producers attempted to raise their quotations, and others increased the prices of aerospace-grade sponge titanium products. Due to the relatively stable supply of aerospace-grade sponge titanium and favorable downstream demand, its prices rose smoothly. The main users of grade one sponge titanium were in the industrial sector, with limited capacity to absorb higher prices. After the price reached 50,000 yuan/mt, downstream enterprises were unwilling to accept any further increases.

In May, the titanium dioxide (TiO₂) market continued its downward price trend, with declines ranging from 300 yuan/mt to 500 yuan/mt, and market quotes were relatively chaotic. At the beginning of May, under the dual pressures of weak end-use demand and high inventory levels, enterprises successively lowered their new order quotes. The listing prices of leading enterprises were reduced by 500 yuan/mt, triggering a chain reaction of price reductions in the market. Enterprises were constrained by both the market downturn and cost pressures, resulting in high inventory levels. To alleviate inventory pressure, nearly half of the enterprises chose to halt or cut production, leading to a significant decline in the market's operating rate. However, the contraction rate of the supply side significantly lagged behind the decline in demand, and the market's oversupply contradiction was not effectively alleviated.

Outlook

In June, the titanium ore market will continue to face a severe situation. As the market enters the traditional off-season, there is little prospect of significant improvement in demand for downstream products in the short term, and titanium ore prices for small and medium-sized miners will continue to be under pressure. In terms of imported titanium ore, due to significant shipping pressure, it is expected that some domestic miners will have room to lower their imported ore prices.

In June, the titanium slag market will remain challenging. Although the high-titanium slag market has some cost support, if there is no significant improvement in demand, prices will continue to be under pressure. In June, the tender prices of large northern plants fell by 300 yuan/mt, leading to widespread losses and production halts among titanium slag plants, further suppressing their willingness to resume production, and the operating rate will remain low. Given the lack of improvement in downstream demand, the acid slag market is expected to continue in a weak and sluggish state, with prices potentially declining further.

It is expected that in the short term, the price of titanium sponge will continue to maintain a phased high level. Currently, titanium sponge enterprises are cautious about increasing production, and the overall market supply and demand situation is relatively stable. Since March, titanium sponge prices have gradually increased, and the pressure for further price increases in the future will also intensify, with relatively limited upside room. In the second half of the year, if some new capacities are put into production, titanium sponge prices may once again face challenges.

In the future, the titanium dioxide market may continue to operate in a weak state. On the demand side, it is difficult to achieve significant improvement due to the impact of the traditional off-season and blocked foreign trade. On the supply side, despite the decline in enterprises' operating rates, the oversupply situation is difficult to reverse in the short term. Supported by high costs, the downward room for titanium dioxide prices is limited. It is expected that in June, the market will continue to adopt a transaction mode of one order, one negotiation.

Import Data Statistics

In April, China's imports of titanium ore concentrates and middling ores were 419,000 mt, up 27.55% YoY and down 12.39% MoM. From January to April, China's imports of titanium ore were 1.776 million mt, up 18.13% YoY.

In April, China's imports of titanium plates, sheets, and strips with a thickness of ≤0.8 mm were 221.5 mt, up 27.97% YoY and 42.74% MoM. From January to April, China's imports of titanium plates, sheets, and strips with a thickness ≤0.8mm reached 480.6 mt, up 26.65% YoY.

In April, China's imports of titanium plates, sheets, and strips with a thickness >0.8mm were 84.3 mt, down 38.08% YoY and 45.45% MoM. From January to April, China's imports of titanium plates, sheets, and strips with a thickness >0.8mm were 380.2 mt, down 21% YoY.

In April, China's imports of titanium pipes were 29.3 mt, down 43.84% YoY and 13.3% MoM. From January to April, China's imports of titanium pipes were 72.1 mt, down 58.28% YoY.

In April, China's imports of other unwrought titanium were 21.3 mt, up 58.04% YoY and 25.39% MoM. From January to April, China's imports of other unwrought titanium were 91.8 mt, up 166.97% YoY.

In April, China's imports of titanium bars, rods, sections, and profiles were 1,868.9 mt, up 1,698.03% YoY and 206.81% MoM. From January to April, China's imports of titanium bars, rods, sections, and profiles were 3,505.7 mt, up 347.89% YoY.

In April, China's imports of titanium wires were 13.8 mt, down 63.35% YoY and 56.6% MoM. From January to April, China's imports of titanium wires were 75.6 mt, down 16.51% YoY.

In April, China's imports of other wrought titanium and titanium products were 51.2 mt, down 38.67% YoY and up 4.68% MoM. From January to April, China's imports of other wrought titanium and titanium products were 174.7 mt, down 27.99% YoY.

In April, China's imports of titanium dioxide were 6,600 mt, down 2.71% YoY and 20.44% MoM. From January to April, China's imports of titanium dioxide were 27,400 mt, down 11.87% YoY.

Export Data Statistics

In April, China's exports of titanium sponge were 979.1 mt, up 436.47% YoY and 134.67% MoM. From January to April, China's exports of titanium sponge were 2,474.5 mt, up 90.05% YoY.

In April, China's exports of titanium plates, sheets, and strips with a thickness ≤0.8mm were 163.4 mt, up 105.6% YoY and 16.67% MoM. From January to April, China's exports of titanium plates, sheets, and strips with a thickness ≤0.8mm were 450.7 mt, up 4.75% YoY.

In April, China's exports of titanium plates, sheets, and strips with a thickness >0.8mm were 496 mt, down 61.32% YoY and 24.8% MoM. From January to April, China's exports of titanium plates, sheets, and strips with a thickness >0.8mm reached 2,273.3 mt, down 40.36% YoY.

In April, China's exports of titanium pipes amounted to 276 mt, up 11.69% YoY and 27.38% MoM. From January to April, China's exports of titanium pipes totaled 973.5 mt, down 1.39% YoY.

In April, China's exports of other unwrought titanium amounted to 49.3 mt, down 77.34% YoY and up 20.38% MoM. From January to April, China's exports of other unwrought titanium totaled 262 mt, down 56.8% YoY.

In April, China's exports of titanium bars, rods, profiles, and special shapes amounted to 529 mt, down 38.5% YoY and 52.73% MoM. From January to April, China's exports of titanium bars, rods, profiles, and special shapes totaled 3,111 mt, up 4.43% YoY.

In April, China's exports of titanium wire amounted to 239.6 mt, up 79.94% YoY and 131.38% MoM. From January to April, China's exports of titanium wire totaled 545.4 mt, up 1.38% YoY.

In April, China's exports of other wrought titanium and titanium products amounted to 482.9 mt, up 42.01% YoY and 5.03% MoM. From January to April, China's exports of other wrought titanium and titanium products totaled 1,736.4 mt, up 22.09% YoY.

In April, China's exports of titanium dioxide amounted to 148,000 mt, down 5.96% YoY and 20% MoM. From January to April, China's exports of titanium dioxide totaled 649,000 mt, up 0.32% YoY.

Zirconium Market Analysis

In April, China's imports of zircon sand amounted to 21.78 mt, up 25.71% YoY and 7.72% MoM. From January to April, China's imports of zircon sand totaled 845,000 mt, up 31.39% YoY.

In April, China's exports of zirconium oxychloride amounted to 5,883 mt, down 0.52% YoY and up 73.35% MoM. From January to April, China's exports of zirconium oxychloride totaled 15,497.3 mt, down 6.08% YoY.

In April, China's exports of zirconium carbonate amounted to 1,333.8 mt, down 38.05% YoY and 27.67% MoM. From January to April, China's exports of zirconium carbonate totaled 5,833.9 mt, down 17.59% YoY.

In May, the supply of zircon sand continued to increase, while end-use consumption showed no improvement, leading to a continued decline in domestic zircon sand prices. At the end of May, the price of imported 66% high-grade sand was approximately $1,850/mt, and the price of domestic 65% zircon sand was approximately 12,300 yuan/mt.

In May, the real estate market remained sluggish, zircon sand prices continued to fall, enterprises faced significant inventory pressure, and the price of zirconium silicate continued to decline. At the month-end of May, the price of ordinary zirconium silicate was approximately 12,300 yuan/mt.

In May, the mainstream quotations for zirconium oxychloride from leading enterprises ranged from 14,000 yuan/mt to 14,500 yuan/mt, with mainstream quotations around 14,000 yuan/mt. Some enterprises, eager to sell their products, offered prices lower than the mainstream prices.